Last week, you built your Career Balance Sheet. You listed every problem you've solved. You put real numbers on your impact.

Maybe you automated processes and saved $1.5M. Maybe you closed a deal worth $20M in ARR. Maybe you cut sales cycles from 6 months to 8 weeks.

But here's the first principles question: What's the fundamental truth underneath all those achievements?

Strip away the job titles. Strip away the company names. Strip away the activities.

What's left is your pattern. Your superpower. Your professional brand.

Not a vague statement like "I'm a strategic leader." A precise statement built from fundamental truths that makes someone say "I need that person right now."

Look at your Career Balance Sheet. All your achievements are there. Now look for the pattern.

What's the thread that runs through everything you've done?

Let me show you with real examples.

The CFO who raised Series A ($5M), Series B ($15M), Series C ($40M), and took the company public ($200M valuation).

Pattern: Takes companies from early stage funding to IPO.

Professional brand: "I'm the CFO who takes companies from seed to IPO."

The CRO who joined at $2M ARR, built the sales team from 3 to 15 people, and left at $22M ARR.

Pattern: Scales revenue in the $2M to $20M range.

Professional brand: "I'm the CRO who scales revenue from $2M to $20M ARR."

The Product Leader who inherited a feature with 15% adoption, rebuilt the feedback loop, redesigned onboarding, and hit 82% adoption.

Pattern: Makes products people actually use.

Professional brand: "I'm the Product Leader who took feature adoption from 15% to 82%."

See the pattern in these patterns?

Each one has three elements:

Not activities. Not responsibilities. Outcomes.

Now you need to know if your brand actually resonates.

Think of it like a doctor testing a diagnosis. You have a hypothesis. You run tests. You see if you're right.

Create three variations of your brand statement. Test them.

Update your LinkedIn headline with Version A. Give it two weeks. Track profile views, connection requests, InMail messages.

Switch to Version B. Another two weeks. Compare the numbers.

Test in real conversations. When someone asks what you do, use your brand statement. Watch their reaction.

Do they lean in and ask questions? That's resonance.

Do they nod politely and change the subject? That's not working.

After 4-6 weeks, you'll have data. One version will clearly outperform. That's your signal. That's what the market wants.

Your professional brand tells you exactly who to target.

"I'm the CFO who takes companies from seed to IPO" → Target companies that just raised Series B or C. They'll need IPO prep in 18-24 months.

"I'm the CRO who scales revenue from $2M to $20M ARR" → Target companies currently at $2M to $5M ARR who just raised Series A.

"I'm the Compliance Head who gets startups their license" → Target pre-license companies that just raised funding.

You're not searching "fintech jobs."

You're searching for companies at the exact stage where they need your exact capability.

Create a hit list of 10-15 companies you've researched deeply. For each one, track:

Not 200 random applications. 10-15 companies where you've done your homework.

This is precision targeting, not spray and pray.

Before: "Hi, I'm applying for your CFO role. I have 15 years of finance experience. I'm detail-oriented and a strong communicator."

After: "Hi, I noticed you just closed your $40M Series C with Sequoia. Based on their portfolio pattern, you're likely 18-24 months from IPO conversations. I'm the CFO who's taken three companies through that exact journey. The biggest challenge is always audit readiness 12 months before filing. I'd like to discuss what you're seeing."

Which one gets a response?

The second one shows you understand their business. You've done your homework. You're not applying - you're offering to solve a specific problem they have right now.

That's the difference between 1% response rates and 60% response rates.

You have your Career Balance Sheet. Now turn it into your professional brand.

Extract the pattern. Write it as one quantified sentence. Test it. Find companies who need exactly what you do.

Then reach out with precision, not desperation.

Listen to the full episode of Finding Your Next Role in Fintech for the complete framework, testing methodology, and research strategies.

Episode 1 - The Career Balance Sheet framework

Episode 3 - How to use professional networks

Download the Professional Brand Worksheet and Problem Portfolio template to build your brand and target list.

Building a fintech leadership team?

Most people treat networking like fitness. They lie on the sofa for three years eating chips and drinking beers, watching sport instead of playing it. Then they wake up one day, realize they've gained 20kg professionally, and can't climb the career stairs anymore.

Sound familiar?

You go three years without talking to anyone in your network. Then you panic. Coffee meetings everywhere. LinkedIn messages flying. Desperate energy everywhere.

Here's the problem: You wouldn't train for a marathon by doing nothing for three years, then running 100km the week before the race. Your network works the same way.

When I launched Tier One People 10 years ago, I had 5,000 contacts in my database. Most people would email all 5,000. Spray and pray.

I did something different.

I filtered that list down to 98 people using a specific method. That was my critical 5%.

Those 98 people generated over 95% of my business results in the first year.

Here's the truth: 95% of your results will come from 5% of your network.

Not 10%. Not 20%. Five percent.

Break your network into three tiers:

Tier 1: Former bosses and colleagues who are now in hiring positions. People who know what it's like to work with you and can now make hiring decisions.

Tier 2: People with massive networks. Clients, law firm partners, investors, VCs, board members. People whose job is knowing other people.

Tier 3: Everyone else.

Your critical 5% is Tier 1 plus Tier 2. That's your focus.

Here's what everyone else writes:

"Hi X, how are you? Not sure if you heard but I was made redundant the other day. I'm on the market and I've attached my CV. Would love to catch up for a coffee, my shout."

See the problem? You're leading with your need. You're asking for too much. And you're valuing their time at the price of a flat white.

Here's what works:

"I'm thinking about a few possible career paths and as someone I highly rate and whose opinion I trust, I wondered if you had two minutes to chat. I know you won't sugarcoat things."

Two minutes. Not coffee. Not lunch. Not a job.

Two minutes is incredibly hard to say no to.

When you ask people for two minutes, they ask you for coffee.

When you ask them for their honest opinion, they give it. I've never met a single person who didn't enjoy telling me what they really thought.

But here's where the magic happens:

As soon as someone says "I think you should do X," they feel responsible for helping you do it. And they follow up with "Let me introduce you to Y."

Now you get another meeting with an influential person who could hire you. And you arrive pre-endorsed.

This is the compound effect. One conversation generates 1-2 warm introductions. Those introductions generate more conversations. Those conversations generate opportunities.

When I sent my two-minute message to 98 people, I had 60 meetings confirmed within 3 days. That's a 61% response rate.

Not because I'm special. Because the message made it easy to say yes. And because I focused on my critical 5%.

Years ago, I watched a sales rep push past me at a networking event and try to force his business card on a CEO. She calmly put her hands behind her back and said:

"You don't need to give me that. What you need to do is get someone I know and trust to give it to me."

That taught me everything about networking.

Stop trying to build trust from scratch with cold emails and forced connections. That takes months or years.

Instead, leverage the relationships you already have. When your former boss introduces you to their colleague, you don't start at zero. You start at 50%. You borrow their trust, their credibility, their relationship capital.

That's why warm introductions are 10 times more powerful than cold outreach.

Your critical 5% might be 10 people. It might be 50. It might be 200. The number doesn't matter.

What matters is this: Stop trying to network with everyone. Start identifying your critical 5%.

Better contacts beat more contacts every single time.

Listen to the full episode for the complete T1/T2/T3 framework, exact email templates, and the two-minute call structure that turns conversations into opportunities.

Download the Network Activation Worksheet with email templates, conversation scripts, and tracking tools.

If you're struggling to land a job in fintech here in Australia, you're probably approaching it the wrong way.

Most people searching for fintech jobs treat the hiring process like they're applying for permission to work. They craft the perfect resume, polish their LinkedIn profile, and hope someone notices them among hundreds of other applicants. But here's the uncomfortable truth: in today's competitive fintech job market where candidates need an average of 294 applications to secure employment, being "qualified" isn't enough anymore.

It's time to stop looking for happiness and start solving problems.

In Episode 1 of our new video series, Finding Your Next Role in Fintech, we introduce a framework that flips the traditional fintech job search on its head: the Career Balance Sheet.

Just like a company's balance sheet shows assets and liabilities, your Career Balance Sheet demonstrates the tangible value you've created throughout your career. But instead of listing job duties and responsibilities, you're documenting concrete problems you've solved and quantifying the value you've delivered.

This isn't about exaggeration or spin. It's about recognising that every role you've held, every project you've completed, and every challenge you've overcome has created measurable value for someone. Your job is to articulate it clearly.

When you position yourself as a problem-solver rather than just another applicant in the fintech jobs market, three things happen:

In the episode, we walk through four detailed examples across different fintech roles. These real-world scenarios show how professionals in various fintech jobs have documented their value:

Each example demonstrates a simple but powerful formula: Problem + Solution + Quantified Value = Your Competitive Advantage

This Career Balance Sheet approach works across all fintech jobs, including:

No matter what type of fintech job you're pursuing, documenting your value creation is what sets you apart from other candidates.

Ready to document your value? We've created a free Career Balance Sheet worksheet to guide you through the process.

The worksheet helps you:

Download the Career Balance Sheet Worksheet (Free PDF)

In 2025, fintech jobs in Australia have become more competitive than ever. With sustained economic pressures and increased application volumes, standing out in the fintech job market requires more than just qualifications, it requires proof of how much value you create.

The candidates getting hired aren't necessarily the most experienced. They're the ones who can clearly articulate the problems they solve and the value they create. This approach gives you a competitive edge.

Understanding what fintech employers are really looking for (problem-solvers who can demonstrate measurable impact) is the key to landing your next fintech role.

This blog post only scratches the surface of what we cover in Episode 1. In the full video, we walk through:

Finding Your Next Role in Fintech is a 5-part video series that applies business methodologies like first principles thinking, lean startup, design thinking, enterprise software sales frameworks and go-to-market strategies to your Fintech Job Search. Whether you're pursuing permanent roles or exploring fractional opportunities, this series will transform how you approach the fintech job market.

Coming Soon:

At Tier One People, we specialise in connecting exceptional fintech talent with financial technology companies across Australia and globally. Whether you're searching for fintech jobs in risk management, compliance, payments, lending, or business development, we understand what employers are looking for.

If you're ready to position yourself as a problem-solver rather than just another applicant in the fintech job market, we'd love to connect.

Explore Fintech Jobs | Subscribe to Our Newsletter

Dexter Cousins is Managing Director of Tier One People and host of the Fintech Chatter Podcast. With over 25 years in recruitment, he works at the intersection of AI and fintech, helping shape Australia's position in the global fintech ecosystem.

How hard is it to find a job in Fintech in Australia right now?

Fintech jobs in Australia are highly competitive in 2024-2025, with candidates needing an average of 37 applications to secure employment. The market has seen increased application volumes due to economic pressures, making it essential to differentiate yourself through proven value creation rather than just qualifications.

What skills do employers look for in fintech jobs?

Fintech employers prioritise problem-solving abilities and measurable business impact over credentials alone. They look for candidates who can demonstrate how they've created value through cost savings, revenue generation, risk mitigation, or process improvements in previous roles.

How can I stand out when applying for fintech jobs?

Use the Career Balance Sheet framework to document specific problems you've solved and quantify the value you've created. Instead of listing job duties, show concrete results like "reduced compliance processing time by 85%" or "generated $20M in new ARR."

Are there remote fintech jobs available in Australia?

Yes, many fintech companies across Australia now offer remote and hybrid fintech jobs, especially in technology, compliance, and business development roles. The Career Balance Sheet approach works equally well for remote fintech positions.

What types of fintech jobs are most in-demand?

Currently, high-demand fintech jobs in Australia include compliance and risk management specialists, AI/ML engineers, payments specialists, business development professionals, and product managers with fintech experience.

I’ve recently seen the term Fractional Executive marketed as the panacea to a fintech founders growth challenges. And whilst the term seems to be gaining steam on LinkedIn, it is yet to fully hit mainstream.

Over the past decade I’ve been a big advocate for startups engaging executives on a project basis to deliver specific outcomes. I even coined the term ‘Gig Exec’ back in 2016.

The concept is not new, in 2008 I noticed a number of my network switching their title from 'Interim' to 'Consultant' and in 2012 from 'Consultant' to 'Virtual Executive'

Where a 'Virtual' or 'Fractional' Executive may differ from a traditional interim executive is they have asynchronous clients.

Sadly my research indicates that over 80% of founders were/are unhappy with the results when they engaged a ‘Fractional Executive’

On the surface it seems like a great idea, tapping into an experienced executive for a fraction of the cost. But there are some real challenges prohibiting successful outcomes.

So if you are thinking of engaging or thinking of a career as a Fractional Exec, here are some thoughts to ponder:

1. Fractional execs charge time but are measured on outcomes

2. Fractionalised means your focus is on several missions, not on one mission. Which often results in conflicts delivering client outcomes

3. Startups are demanding, like babies - if you have 3 clients it's like having triplets - the challenges compound

4. Fires 🔥 have to be extinguished immediately- a client can't wait for your scheduled day in the office or until you log on.

5. Our research indicates presenteeism is essential for the creative phase of company building. People need leadership and as yet the human race is still figuring out how we do that virtually.

6. Mental exhaustion- startups present complex problems that must be solved under intense pressure. Multiple clients means multiple problems - again there is a compounding effect leading to rapid burnout.

7. People overestimate their ability to deliver and clients underestimate the size of and cost associated with the problem. This creates big expectation gaps.

8. Which leads to expectation gaps. A client will expect you to deliver the same outcome as a full time employee and usually expects the same level of commitment.

9. Lack of experience in startups. Many fractional execs come from corporate land where they are one dimensional and political. Under pressure they don't deliver, make mistakes and then blame other people or simply go awol

10. My Linkedin research shows less than 10% of fractional execs have more than 3 year's experience working this way. Startups have very different challenges in 2023 and many fractional execs may not have experienced these challenges in their careers.

10.1 Trust or lack of - from board and founders

Originally published on Startup Daily

Ask any founder their top three challenges, and talent is likely to feature amongst them.

Record low unemployment, closed international borders, the great resignation, remote workers, soaring salaries and a global skills shortage have created the most complex talent crisis in the modern era.

Many business leaders I speak to feel helpless right now. But could things be about to change?

I’m a recruitment veteran. I’ve recruited through the dotcom crash and the GFC. I should have recruited through my third crash in 2020. Now all the indicators suggest we are headed for a global recession in 2022.

What makes me so confident? Whilst we are not technically in a recession, every major economic downturn I’ve seen has been preceded by a red hot talent market.

1999-00 My phone and fax never stopped! Then the tech wreck happened. Ice cold jobs market.

2007-08 Everyone wanted to work at an investment bank for triple their salary and got it. The GFC hit. Ice cold jobs market.

2020-22 Has been the hottest talent market on record! I never thought I would see a day when people would refuse to work in an office two days per week. Or entry-level developers would be paid $150,000. Yet here we are.

Talent markets are like any other market. Price is determined by supply and demand.

If the market gets inflated too much it creates a bubble. Then the bubble bursts.

Let me take you back to March 2020. The markets tanked 30%, the world shut its borders and went into lockdown as a global pandemic put us all on red alert. Australia soared to 9% unemployment in a month! Businesses shut and we faced the greatest economic crisis of our lifetime.

The only way for most businesses to operate and survive during the lockdown was to go fully digital. Some were prepared for it, but most weren’t. The demand for tech talent soared, and at the same time borders were shut. For a short time, it looked like the demand for tech talent could be met locally.

Most tech startups had 3 -12 months of cash runway – at one point it looked like we could lose up to 75% of the startup ecosystem.

The government stepped up to provide support and stimulus in Jobkeeper. And by July 2020 the economy was pumping again. Tech valuations soared, Afterpay hit $150 and made the ASX 20. VC poured billions into tech startups. Series A rounds quadrupled. The tech ecosystem was flush with cash.

But the demand for tech talent got greater and greater.

The cashed-up tech companies smelt blood and aggressively poached talent from tech startups, offering 30-50% pay increases in some instances.

The large corporates, banks and telcos also targeted talent from startups, offering big salaries to make up for no equity.

The only way for startups to fight back was to offer more money. Or lose experienced staff for less experienced people. The only problem is that salaries rose across the board. Entry-level developers are now earning more than startup founders and leaders.

The tech talent shortage has created the biggest talent bubble in my career.

Stop hiring.

Don’t want to pay $8 for lettuce? Stop eating lettuce.

Fairly soon you’ll find you can do without and quickly the cost of lettuce is back to $2

The same dynamics work in the talent market.

If 2021 was the year of “Growth at all costs”, then 2022 is the year of “Cut costs at all costs”

Since the beginning of 2022, we’ve seen Tesla, Paypal, Coinbase, Robinhood, Klarna, and Netflix all make job cuts of 10-20%

We’ve also seen high-profile startups like Fast run out of funding and shut their doors, leaving 300 people without a job.

And as these job cuts are happening, we are now hearing of headcount freezes at Meta, Uber, Lyft, and Twitter with more to follow.

In the US talk of the great resignation is being replaced with talk of a great recession.

Australia often lags behind the US, usually by six months. Over the last two months, I began to hear of staff layoffs at Envato, Brighte, Banxa, HealthMatch, Una, Booktopia, Bizpay and other tech startups.

Last week Volt Bank announced it had run out of capital and would close its doors, with 140 employees losing their jobs.

Tech valuations have tanked with some high-profile Aussie tech firms down 90% from 12 months ago.

This puts extraordinary pressure on any business to cut costs and make job cuts. With severe drops in valuation right across the tech sector, it also means capital is drying up.

The sector is not as attractive to investors as it was 12 months ago.

Sure some investors are out there looking for bargains, but with rising interest rates, the appetite for high-risk investments is waning.

And with a global recession on the horizon, investors are in no hurry to rescue companies that may be insolvent in months.

It’s not only startups that are impacted by recessions. Australia’s corporations will implement cost-cutting measures to ensure they deliver shareholder returns.

Historically profits are delivered in a downturn through restructuring (ie cutting headcount) and axing expensive technology projects.

NAB recently announced that 100 tech roles would be offshored to India. The unrealistic salaries demanded by inexperienced developers and engineers may have prompted NAB and many other Australian businesses to hire offshore workers.

Commonwealth Bank employs 4400 software developers. That’s a lot of software developers. Imagine what a 10% headcount reduction does for the local talent market?

According to the Tech Council, there are currently 860,000 Australians employed in the tech sector.

A 10% cut across the industry over the next 3 months means 86,000 people looking for a job.

Even if Australia avoids a recession, it’s likely the US and Europe will not.

Now that borders have opened up we once again have the option of hiring international talent. Australia is a very attractive proposition for tech talent. The tech scene has matured considerably and the lifestyle is unbeatable.

Going back to the lettuce analogy, most founders weren’t prepared to pay $8 per head. Instead, they sought alternative markets and have built strong links to Eastern Europe, India and Asia where highly experienced tech talent can be hired at a 50% discount to a junior developer in Australia.

Early-stage startups have embraced remote working, accessing some of the world’s best engineering and tech talent from the US and UK. It is only a matter of time before large corporates do the same.

In the last two years, we’ve seen the emergence of platforms making it much simpler from a legal and compliance perspective to hire and pay offshore workers. And while there have been teething problems, as businesses become more accustomed to working remotely, the cost benefits and the ability to access broader talent markets put increasing pressure on the local talent market.

Every time I have experienced a global downturn the talent market has gone from red hot to ice cold in the space of a few months.

There’s every possibility that the supply/demand ratio which has inflated the talent bubble we find ourselves in could burst very quickly.

Not quite. Back in 2005 as one of Australia’s first ‘digital’ recruiters, it became very clear that due to the pace of technology innovation the supply/demand metrics would never be balanced.

The reality is that being at the forefront of innovation means using the latest technology. Most education facilities lag behind the demands of commerce and industry. My solution back then is the same as today, indeed, it’s essential today and far more realistic.

Companies MUST change the way they go about identifying and hiring talent.

When hiring for tech startups our emphasis must shift from hiring people based on programming languages to hiring people based on their propensity to learn new programming languages.

With online learning readily available, people with a strong desire to learn new skills can and do. Successful tech companies are those who consistently identify these traits in people when hiring.

One of the biggest benefits of closed borders this last two years is that Australia has developed a domestic workforce capable of launching and scaling tech startups.

We must harness that IP and pass it on to the next generation of talent. Instead of discarding resumes because a person doesn’t have Kotlin, we need to look at what they’ve accomplished, and what they have built and seek to utilise that experience.

But if we continue the hiring practices that got us here – we’ll just see another talent bubble as soon as the next recovery begins.

An opinion piece by Dexter Cousins, Managing Director of Tier One People.

In late 2022 Chat GPT seemed to come out of nowhere, the truth is the technology is 7 years old and advancing at a rapid rate. Companies have been developing AI tools for decades, and in the last 10 years we've seen a huge increase in the adoption of AI in business.

So why is everyone suddenly scared that AI is going to take their job? I originally wrote this article back in 2017 and have come back to update it several times.

It is a question I am asked everyday. Now if you had asked me three years ago my answer would have been 'no.'

Today I am not so sure, in fact I am convinced technology will replace up to 80% of jobs in banking.

While it is just a theory, it is not one I have plucked up from thin air. Nor is it based on wild claims about the capability of AI. This post is not intended to alarm people, but there are forces at play that when I follow through to a possible conclusion, there's a very real danger to jobs and our careers.

Since 2012 I have been absorbed by the changing nature of work. My interest was piqued when I heard about a company called 'Freelancer', a platform connecting knowledge workers around the world.

Ever since I've spent much of my time researching and analysing the disruptive nature of technology, AI and robotics in the workforce. And yes I am worried about my own existence as a managing director of a recruitment business.

And this fear drove me to reinvent my own career, business and approach just to remain relevant. Ultimately I set out to create a business that was recession-proof and could be operated from anywhere in the world with a smartphone and internet connection.

Since Covid hit and remote working has been forced upon us, the term ‘The future of work’ is repeatedly used - but the future is here and has been for some time.

What we are seeing now is a tidal wave of change that has been building up for decades, multiple forces are converging that threaten very rapid change which humans are struggling to keep pace with.

In this two part piece I'll cover the forces and share why I believe they will make 80% of banking staff redundant.

There's a lot of debate about Neobanks and if they will succeed. There seems little concern from the incumbent banks that Neo's will ever get the scale to threaten their profits. I feel this is a rather short-sighted and narrow view of the threats.

Australia’s leading bank, Commonwealth Bank, was founded in 1912. It serves approximately 10m customers across retail and business banking mainly across Australia. The bank employs approximately 52,000 people and in 2020 made a net profit of Au$7.3bn or a profit of Au$146,000 per employee

As banks go, they are at the forefront of digital innovation and easily in the top 10 banks globally when it comes to digital. They took the bold step of replacing their core banking system in 2008 and are currently in the process of moving 95% of technology and apps into the public cloud.

Revolut. Some would argue is not a bank although it does hold a European banking license and is in the process of applying for a UK banking license. Launched in 2015, in just six years Revolut has gained 14m customers with operations in the UK, Portugal, USA, Japan, Singapore, India and Australia.

It offers customers low cost international transfers, access to gold and silver, cryptocurrency, free share trading and in the UK also offers business accounts. Revolut develops products and ships features at a lightning pace, operating more like Amazon than JP Morgan.

Revolut currently employs approximately 2000 employees and is now operating at a profit.

What is not clear at this stage is if Revolut's model will generate big profits like CBA. In order to be as profitable as CBA per employee, they will need to generate Au$292,000,000 profit.

Revolut does not yet offer lending products, which are the most profitable products in any retail banks portfolio. But when Revolut does start lending, how many additional people will they need to employ?

Definitely not 50,000.

Is Revolut a one off? No, in Hong Kong, Welab has approximately 800 staff and serves 40+ million users/customers.

As more companies like Revolut and Welab gain momentum, increase revenue and exponentially increase profit, surely boards have to question why 52,000 are needed to run a bank?

In Australia we have witnessed 3 CEO’s lose their job in the last two years, all to mishaps in risk and compliance and ultimately human error/interference. The logical conclusion to draw - if processes can be automated to remove the potential risk of human error they will be.

Most banks are listed on a stock exchange, meaning their no1 goal is to generate profits for shareholders. And in order to remain profitable incumbent banks will need to replace people with technology. Shareholders expect returns and dividends and every CEO is incentivized to deliver.

When you already have the lion's share of the market, the only way to deliver more profit is to cut costs. And people are usually where the biggest cost savings can be found.

Many banks are focused on replacing legacy systems and moving to the cloud. Covid19 has accelerated this trend. But could a move to the cloud lead to job losses and displacement?

We have to anticipate that more efficient technology will lead to job cuts, particularly for those who's jobs are based on data input and spreadsheets. But there are greater implications

Commonwealth Bank is ahead of the curve having replaced the core banking system and moved to the public cloud. Matt Comyn the CEO is intent on delivering a new experience for customers. And to help he is bringing in the very best talent from the startup and Fintech world.

Developers, engineers, cybersecurity, blockchain, data science. The list of talent suggests CBA identifies itself as a silicon valley tech giant, much like Google, Facebook and Netflix.

As more and more banks replace legacy systems and move to the cloud their demand for similar skill sets will increase. We are seeing this with other digitally savvy banks like JP Morgan and Goldman Sachs.

The demand for these skills is high, but supply is low, especially if you look locally. Here in Australia we see comparably average software developers with 2-3 years experience commanding $200,000 per year. In the past many banks have made do with local talent. Now they are looking globally for the very best talent in the market.

If you go to India or Eastern Europe you can get incredible developer and engineering talent talent for a fraction of the cost. With a move to cloud banks realise many of their staff can work remotely, which means technically a job can be done anywhere in the world.

This potentially threatens local jobs in two ways.

2. If a job can be done remotely, technically it can be done anywhere in the world, meaning cheaper labour is available. Will lower skilled workers miss out on the jobs they are qualified for to overseas talent who can perform the same tasks at a fraction of the cost?

There’s a recent trend where offshore jobs have been brought back onshore. One area we’ve seen this most is in customer service, especially since Covid. Bank branch staff have been repurposed as customer service/contact centre staff.

This is good news in the short-term. But there’s a looming risk to jobs. We work with several Ai companies who work with banks and are in the process of automating customer service. Working closely with the customer service staff, actions are input into Ai/Machine learning models and emulated.

I’ve personally seen trials of the technology and it is scary how good it is for dealing with general enquiries. I was on hold for 3 hours to my bank last week for a simple inquiry that’s still not resolved, waiting in a queue for a human to answer!

Artificial intelligence is being adopted in Customer Service, Risk, Pricing, Compliance, Finance, Treasury, basically every area of the banking industry.

While it will never replace humans completely it will take away many of the mundane and repetitive tasks. It’s feasible that a department of 50 could become a department of 5 SME’s supported by a data scientist and Ai.

The promise of CDR (Consumer data Right) is some way off. It’s an ambitious plan to give consumers the right to use their data for their benefit. Imagine applying for a mortgage and getting unconditional approval in minutes. That is the promise of open data.

Initial progress is slow, but don’t underestimate how fast things will move once there is traction. Tier One People is working with well-capitalised startups with a vision to completely disrupt lending.

The applications for open banking threatens jobs on many levels.

The first two jobs at risk are credit and underwriting. With access to my entire past 10 years of spending and online data, credit risk models will be able to give a decision instantly. Just ask anyone applying for a home loan right now if this is something they want. People are losing deposits on houses because it is taking banks 3-4 months to give a decision on an application.

Now imagine a world where you are instantly given a decision and approved. This potentially takes away the need for mortgage advisers, underwriters and credit assessors. And because it is all automated with audit trails, there’s no need for compliance either.

My kids are 10 and 8. They love video games and can tell you everything you want to know about Neobanks. They closed down their school bank account recently.

“How dare a bank expect me to turn up to school with cash, fill in a deposit form and not let me access my money when I need it”

Now they have a Spriggy account (with cool star wars cards) and Revolut kids accounts. My mum and siblings (living overseas) regularly send the kids money to their Revolut accounts. It hits the account in 30 seconds with no international fees! No waiting 4 days and giving 10-20% to the bank in fees and conversion charges.

They spend most of their money on Avatars in a game called Roblox. You may have heard about it, the company just listed on the NYSE and the share price pretty much doubled.

About half of American kids under 16 are on the platform! So what does this have to do with banking? Quite a bit actually.

First of all the game has its own digital currency, Robux. You can use Robux to buy avatars and play games which other people build. You can even build your own games and get paid Robux when people play your game.

The world my kids are growing up in is a one where they don’t trust banks, they don’t see a need for banks and they are very comfortable with digital currencies and storing them in digital wallets.

We are living in a world where businesses are built almost overnight if they fit the needs of customers. If they don’t, they go bust just as quickly. Blackberry is a great example.

There is no way my kids will tolerate being on hold for 3 hours because of legacy system problems. They will just close the account and go somewhere better.

It is this shift in customer behaviour that potentially poses the greatest threat to banking jobs, mainly because banks are in danger of losing their relevance.

When I first started working, I was paid in cash. I never used nor needed a bank account until my employer began electronic transfers of salaries.

But let’s say my kids choose to be paid in Robux or Bitcoin, like the Basketball star Russell Okung. It goes straight to a digital wallet and maybe held in a cold storage wallet. What kind of impact does this have on bank deposits and their capital adequacy?

We have seen the first glimpses of the changing behaviours of customers with the rapid decline in new credit cards. Instead people are choosing BNPL products with interest-free credit options instead of high-interest cards.

As we move to a negative interest rate scenario, it will cost customers to keep their cash in a bank, will we see deposits shift into digital currencies and gold?

If banks get into capital adequacy trouble, will we see consolidation and further job cuts?

In conclusion banks need to evolve like every other industry and technology will disrupt the model. It is up to us as individuals to recognise and anticipate the changes and keep relevant. This requires reinvention and a consistent focus on personal development.

In the next post I’ll share my thoughts on what the future of banking will look like, the skills in demand and how you can reinvent yourself to remain relevant.

We live in a digital world - yet many of the processes and systems we use are stuck in an analog world. None more so than recruitment. Despite rapid technological advances this century, the process of hiring has remained largely unchanged over the last 100 years. No part of the hiring process causes more debate than the resume.

This is a question I am asked every day. And everyone has their own answer.

Many people are even questioning if we need resumes at all.

You may think of the resume as a record of work so why bother when we have LinkedIn?

But the origins of the resume were as much a marketing tool as a record of work.

So where did the resume originate?

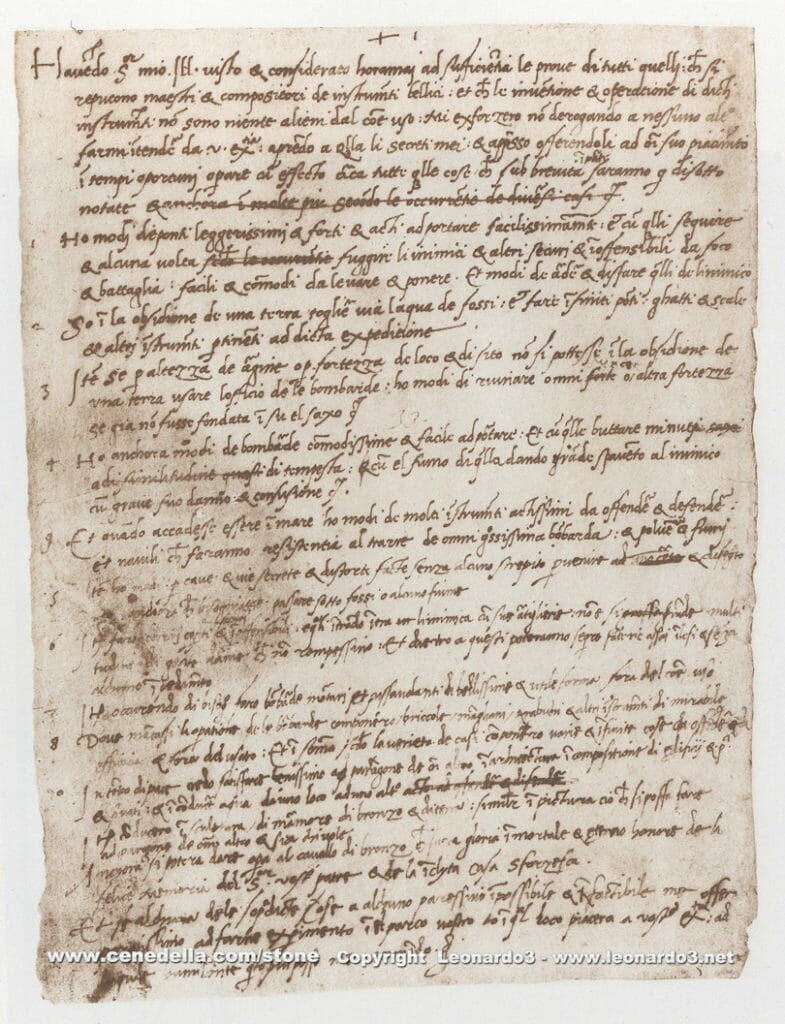

In 1482, a 30-year-old Leonardo Da Vinci wanted to work in the city of Milan as a town planner/architect. So he sent a letter to the Regent of Milan, outlining his skills and experience.

The resume was born!

At the time of Da Vinci, there were obviously no job boards, no recruitment agencies, no LinkedIn, no internet, no video, no phones.

LDV didn't even have a job he could apply to. So how did he pique the interest of the Regent enough to get a job?

Here’s the clever thing LDV did with his resume. Rather than just list the things he had done, he listed 11 ways he could improve the city of Milan with examples to back it up.

Marketing 101 - Identify a problem, present a solution and describe the value it creates.

So not only was Leonardo Da Vinci a supremely talented innovator, engineer and artist, he was also a highly gifted marketer!

The regent of Milan didn't receive hundreds of resumes. He only received one and it was unique!

Today your resume is amongst millions being submitted to job boards and recruitment agencies on a daily basis.

A 2018 study revealed recruiters take on average 7.4 seconds to decide if you are a fit or not.

How do you get your expertise across in a few pages in just 7.4 seconds? Clickbait?

Not quite but if you look at the science behind a clickbait headline it is there to draw the reader in. Then provide more detailed information.

So should your resume be more like a landing page?

Now is the time to innovate, ditch the resume, get with the program and stop relying on a tool that’s over 500 years old.

But everyone demands a resume I hear you say. Of course, they do.

At the time, the only medium LDV had available to showcase his skills and expertise was writing.

But you have video, podcasts, blogs, websites, GitHub, Twitter, LinkedIn, Instagram, Club House, Newsletters. The list of possibilities to convey your skills and expertise is endless!

If Da Vinci followed conventional advice, he'd spend months trying to figure out how to distil his vast experience into two or three pages.

Here’s a few things I think LDV would do to market himself in 2021.

And it should be. If you think of yourself as a business is it acceptable the only way you would promote your business is through a 3 or 4-page brochure? Do companies even have brochures today?

If you are struggling to get all of your experience into a resume, that’s because it is impossible.

Remember we are in the data/digital age. A written 3-page document holds less than a megabyte of information. A video file contains hundreds of megabytes!

Instead of ‘A picture paints a thousand words’ - ‘A video paints a billion words’

If you don't think this is relevant just look on LinkedIn and Twitter and you will see the competition you are up against. There are people creating a personal brand and doing a great job of marketing themselves. To the extent that the work comes to them.

Yes, you do need a resume, but only as part of a multi-channel marketing strategy.

The debate around resumes concerns me. It seems the vast majority of the workforce believes they hold no responsibility for conveying relevant information in ways that clearly articulate their value to a prospective employer or client.

And it causes me even greater concern when writing a resume is outsourced to a resume writing service. No one can or should do a better job of communicating your expertise and experience.

Would you agree that your ability to present and communicate effectively with words is a critical component of your daily work?

With most of the world operating remotely, it has become more important than ever that our writing skills are up to the task.

The resume was designed for A4 paper. But most people will read your resume on a laptop screen or smartphone (we have the data to back this up)

The A4 format actually works quite well for a smartphone - if you keep the formatting simple.

At Tier one People we’ve put together our design know-how coupled with data to create an optimised one-pager resume. The only thing that is missing is your clickbait headline!

You can download the one-pager for free.

"Whenever we hired tech talent with payments or Fintech experience, they would charge us a premium. Where as you go to India and you have Mastercard, Visa, many of the European Banks and many international Fintech giants with large development teams. The reality is we can offer clients people with 10-15 years experience at Mastercard at a fraction of the cost."

Simon Lee - Patona

Tier One People has partnered with Patona Technologies to offer an affordable tech talent solution, helping Fintech scale not fail. Patona provides highly experienced and skilled tech talent at a fraction of the cost associated with hiring in Australia.

Starting life as a bootstrapped startup, Patona saw amazing success by running the majority of its business from India with minimal investment. Patona now has over 100 staff developing, supporting and scaling Fintech across Australia.

Tier One People is proud to partner with Patona, helping our clients scale affordably. At such a mission-critical time for the industry, we feel cutting costs is essential to keep Fintech innovation alive in Australia.

Managing Partner at Patona is Simon Lee, Co-Founder of Assembly Payments. Simon has built several tech companies and has raised over $70m during his time as a founder. Dexter Cousins interviewed Simon for the FinTech Australia Podcast recently.

"When I was running Assembly, if we hired tech talent with Fintech experience, they would charge us a premium. You go to India and there's Mastercard, Visa, many of the European Banks and many international Fintech giants. All of them with large development teams of highly skilled and educated people. The reality is Patona offers clients talent with 10-15 years experience at Mastercard at a fraction of the cost for someone in Australia with 3 years experience. The talent we have working for us at Patona have built apps and platforms at scale, several times over."

Tier One People and Patona share the same values and vision for Fintech in Australia. We want to see Fintech scale, not fail.

A Fintech leaders no1 challenge is people and the unsustainable salaries demanded by Mid-Snr level tech talent. Candidates with a few years experience demand higher salaries than a founder. Even if a startup can hire overseas talent, people quickly raise their salary expectations once they have minimal experience in the local market.

As an example, we approached a senior architect who wanted $250,000 pa to leave their current role, 12 months ago they wanted $120,000. We don't believe offering skilled migrant Visas is a viable solution right now due to COVID. And we question if it is a long term solution, especially when we see remote working so well for all of our clients.

What Fintech founders in Australia have achieved so far is nothing short of remarkable given the challenges and costs of securing highly experienced tech talent. We believe that by utilising high quality, highly experienced, low-cost outsourced tech talent more Fintech jobs will be created onshore. Put simply we expect this solution will see more Fintech's scale and fewer Fintech's fail.

Australian entrepreneurs are not short of ideas, attitude, drive or intelligence. But they do face tougher challenges around access to talent, capital and local economics that make success more difficult to attain than their UK or US counterparts.

Enabling founders to focus on execution and not on raising capital should result in an increase of early-stage Fintech scaling and building sustainable businesses. Without the need to keep raising equity and diluting their ownership.

Tier One People has tried many different service models and pricing structures to make hiring developers and tech talent more affordable. But we simply can not come up with a better, more affordable recruitment solution than Patona. It makes perfect sense for us to partner with them and offer our clients a much faster and affordable path to growth.

To discuss how we can help you scale affordably .....

“The Revolut Country CEO search took six months. The brief changed 4 times as the company grew from 700 to almost 2000 staff during this time. Customer numbers went from 4m to almost 10m. When a company is growing that fast in a highly regulated sector like Banking, it creates a lot of complexity, meaning hiring becomes complex.”

dexter cousins - tier one people

Often the “Fin” in Fintech would denote a heavy hitter from a bank being a winning hire, right?

In the fast paced environment of Fintech, we have noticed caution on the part of our clients in making such a decision.

The hesitation is bound in stereotypes. Banking is often viewed as a mired in red-tape, compliance (or lack of, in Australia), too many chiefs, too many meetings and nothing getting done. Huge amounts of resources and dollars are thrown at projects that never come to fruition. Whilst their Fintech competitors move with stealth and agility, innovating at much greater speed with minimal resources.

The role of an Executive Search Consultant is to challenge stereotypes and get clients to view each candidate on their merits. The view of not being a team player and rolling up your sleeves is often a misconception in banking, but there are plenty who refuse to conform to the stereotype of a banker.

Tier One People is bolstering our position as the leading Australian Fintech Executive Search firm. Australia's growing FinTech sector has seen a rise in the search for C-suite and leadership talent. Counting Revolut, TrueLayer, 10x, Klarna and Transferwise as some of the many companies seeking our assistance.

A more proactive approach job seekers can take is to look at where your big banking skills can have an impact. Assessing whether a company is at start-up or scale up stage will also aid you in making a successful move to Fintech. Read this article on Fintech Career Advice to gain a better understanding at which stage of growth you are best suited to.

Before embarking on the search it is crucial to take a step back and ask yourself;

“How would I cope moving from a structured and heavily supported environment to a one of a specialist generalist”

The best advice we can give candidates looking to join a Fintech.

"Focus on impact. How many years you have worked somewhere doesn’t excite a founder, showing a founder how you can make/save the company millions of $$ does."

Showcasing your skills in 2020 also requires more savvy than ever before. Looking good on paper doesn’t get cut through anymore. If you are in the market looking to join a Fintech you need to have a plan in place and a goal in sight. You need to utilise all of the tools available, LinkedIn, Facebook, Twitter, YouTube, Podcasts. These are all channels where you get direct access to decision makers, people who can hire you.

You can showcase your skills and achievements, bringing them to life and not being blocked by gatekeepers and recruiters.

Dexter Cousins, the CEO and Founder of Tier One People, has interviewed more than 300 FinTech leaders on the subject of hiring. He firmly believes hirers should consider the lifecycle of a Fintech to assess where the best candidate fit is.

It's very difficult for anyone to move from a corporate job to an early stage startup. But with the rapid growth of tech companies, a startup can become an enterprise in 5 years. Examples include Stripe, Revolut and Australia's Afterpay.

It’s a difficult process identifying the right time for a banker to join a Fintech. The right person can definitely make a significant contribution as the company scales. Often times the right hire is made but at the wrong time, which ultimately means the hire is wrong.

We get inundated with calls on a daily basis from candidates seeking a move to the shiny new world of ‘FinTech’. However, opening your pitch with "hey, I've got 20 years experience in banking, I want to work in FinTech" might not be the best way to impress people.

It's also important to make the distinction between a Finance business and a Software business. Are bankers better suited to a NeoBank or a platform provider. Fintech covers a wide range of businesses and making this distinction can really increase your chances of securing a move.

Judo Bank, Xinja, 86 400 and Revolut in Australia have all hired highly experienced bankers early in their growth. Judo and Xinja are both founded by highly experienced bankers who were driven to change the industry.

FinTech’s are at the cutting edge of innovation with far fewer resources than any bank. The reality is no founder or investor gets excited by somebody with twenty years experience in banking unless they can demonstrate previous success in a startup and they have skills currently not in the business which are mission-critical to success.

The recruitment process to join a Fintech can be almost as intense as the job itself. If you can't handle the intensity of the interview process, it's highly unlikely you will succeed in the job.

The thing to remember is that FinTech founders themselves may not have the breadth of experience in HR or Talent to make critical hiring decisions. Hiring for a startup is often a make or break decision. We’ve watched some companies flourish and others flounder because of it.

For a founder looking to hire, specialist FinTech recruiters are more easily able to identify those candidates who are the ”right cultural fit.” Assessing if someone will relish the challenge of working in a FinTech environment is very difficult using traditional interview techniques. And a specialist recruiter can provide far greater access to Talent than an ad campaign and direct networks, especially in talent short markets.

But to achieve these results a client needs to invite us 'into the tent'.

Being attuned to the changing demands of the business is vital to ensure success when hiring.

“The Revolut Country CEO search took six months. The brief changed 4 times as the company grew from 700 staff to almost 2000 during this time. Customer numbers went from 4m to almost 10m. When a company is growing that fast in a highly regulated sector like Fintech, it creates a lot of complexity. Hiring becomes even more complex.” commented Dexter Cousins.

There is a need for the modern executive search consultant to set realistic expectations with their clients. Being transparent and honest (even though clients may not want to hear what you have to say) is the only way to achieve lasting success. This approach is core to the values at Tier One People. The search for the “blue eyed unicorn" is never a realistic one and usually wastes significant time and business opportunities.

As someone who has been in the recruitment industry since the last millenium, I can tell you we are in unprecedented times when it comes to the job market. Mass unemployment overnight, businesses shut down, workforces banned from their office, I feel like I am living in a Hollywood disaster movie! It calls for a different Fintech Jobs Report this month.

If we take a macro view, then we should rightfully get scared for our jobs. But if we take a micro view, is there reason to be more optimistic?

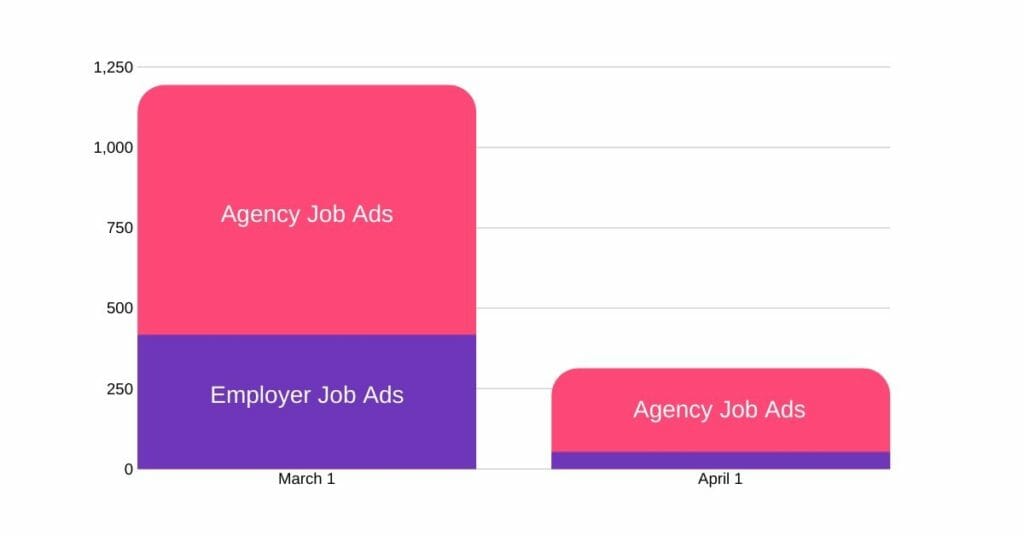

Let’s look at some of the job advert data first. Tier One People track and analyse Fintech job adverts across Seek, Indeed, LinkedIn and Glassdoor.

Most Fintech have put on hiring freezes, some have sadly started to make job cuts.

This is only a guess, but I’m pretty sure that most of the 417 jobs live at the beginning of March remain unfilled. Most of the jobs advertised now are from recruiters and from what I am hearing, it’s desperate times for the recruitment industry. I question how many of the adverts are genuine opportunities.

So, with the market so quiet what can you do to navigate this period? If you are in work, I suggest you become indispensable to your employer. That means increasing productivity and demonstrating where you are CREATING value for the business.

If you do find yourself out of work this is the time to start rethinking your approach to the job search. You should take a read of this article and watch the video.

There will be a rebound in the job market, there always is but when it will happen is anyone’s guess. So we need to focus on the microview to get a sense as to what job opportunities may come about in Australian Fintech.

It’s also worth mentioning that anyone who has been successful in a startup is WAY ahead of the curve when it comes to the next phase of growth and hiring. We are already hearing of many stories where employees are struggling to perform working remotely. The highly structured environment of a corporate does not lend itself well to the new world of work we are now thrust into.

If companies do want to hire purely for skills, then with remote working there is a global talent pool to choose from. Why chose you when there are much cheaper options available?

Put simply, your ability to get shit done and demonstrate where you create value for businesses/customers will be your differentiator.

With a bigger slice of the business banking pie, expect to see increased activity across this space. Government stimulus packages are mainly geared to SME’s. The big 4 banks will be left to administer the lending, but with enquiries in a single day equalling the total annual enquiries, how will the big 4 cope?

We are already hearing of major problems in the UK where less than 900 loans have been approved since the stimulus package was rushed through parliament 3 weeks ago.

The reality is the banks will have to hire people as they don’t have the systems to cope. And they will also have to partner with Fintech to leverage their technology.

Could we see an early adoption of open banking using API’s to connect small businesses directly with lenders? Can Xero, Intuit, MYOB etc provide the access to general ledgers to enable instant decisioning?

The big danger for the Sydney Fintech scene is the huge number of Fintech startups who are under capitalised and not generating significant (if any) revenue. I fear we could see many startups fail during the next 6 months which could have a huge impact on local jobs. I say could, many of these businesses employ 1-10 staff and many roles are part-time, offshore or outsourced.

This opinion piece by Robin Klein, a board advisor at Transferwise gives a fair view point on where government need to focus, it's business triage right now.

On the flip side, those Fintech companies well capitalised and generating revenue could be well positioned as we rebound.

While I expect Australia to face a very long recovery, the companies that do well out of every downturn are the innovators. The Fintech industry has every reason to be optimistic. Especially if we embark on a new world order where monetary systems change, digital currencies become a reality and the world moves to embrace fairer systems of wealth distribution. That may be a decade away, but we all know the shift is inevitable. Is now the time for a true digital revolution?

If you have 30 minutes, watch this video with Ray Dalio - Validation for my optimism from one of the world’s most successful investors!

With Melbourne being the home Revolut, Up, AirWallex, Transferwise, Square, Stripe (all well capitalised businesses) I am hopeful that the Fintech scene there will kick on.

There isn’t quite the concentration of early stage startups as Sydney which means there should be fewer redundancies and hopefully we can keep talent in the industry. Revolut, Airwallex and Square are still advertising open positions.

Product Management - We’ve observed for some time that the challenge of Product/Market fit is a people challenge not a product challenge. The Australian market has never quite got to grips with the role and purpose of a product manager. And unfortunately, right now product management seems to be considered a role in which the responsibilities can be shared amongst tech, marketing and customer success.

Talent and HR - Need I explain?

Sales and Marketing - Any big salary earners not generating revenue are at risk. On the flip side we are seeing demand for revenue generating sales professionals and growth marketing.

Strategy and Innovation - Right now these are considered luxury positions. They may make a glorious comeback as the market comes back, at least historically. But any business hiring innovation people after this downturn is probably close to extinction. I would personally love to see innovation move away from being a department and become a core value engrained in every person in the business - dream on!

Tech and Engineering - It is highly unlikely we will see many if any redundancies of top tech talent. Where we will likely see redundancies are those who are currently overpaid and managed to secure high salaries because of supply/demand market forces vs talent. It’s great being in tech when the market is booming, but the very transactional nature of the tech industry means it can be very tough when the market is down. I’m sure we will see the Big 4 banks and mid-tier banks get excited by the prospect of snapping up people from Fintech when tech redundancies happen.

In response to the rapid escalation of job losses across the Aussie Fintech community Tier One People and FinTech Australia have joined forces to build a Talent Market Place, connecting Fintechers directly to opportunities.

The Market Place is a Private LinkedIn Group where founders and hiring managers can advertise jobs, put out requests for skills and engage talent for contracting.

It is totally free to join for talent and hirers. The only stipulations are you're FinTech Australia member or you've recently been made redundant from a Fintech firm (Australian residents only.)

Those who have recently lost their job and are in the Fintech industry.

To keep talent in the industry and connect immediately available talent with Fintech leaders who can utilise their skills.

People from the Australian Fintech industry and out of work.

We will post daily content, videos and Live chat sessions sharing tips and advice on how to maximise your job hunting efforts. You can connect with hirers direct, no recruitment agencies involved. It's also a great platform to showcase your skills!

You can post active roles, project work, consulting gigs and engage with talent direct in the group.

Developers and Engineers make up more than 50% of all jobs advertised in Australia.

On the face of it, the Sydney Fintech jobs market is going gangbusters compared to every other city with almost 400 advertised positions. But when we analysed the data from advertising platforms including Seek, Indeed, Glass Door, LinkedIn, the real story was nowhere near as impressive.

Find out which jobs are in demand, who is doing the hiring and how using recruiters could be doing your business more harm than good.