Fintech is soooooo hot right now and judging by the amount of enquiries we get at Tier One People, it feels like everyone wants to work in Fintech.

What is a startup? Everyone has their own definition. At Tier One People we have identified distinct phases of growth in a Fintech startup. It is important to make the distinctions as each phase is in effect a completely different business.

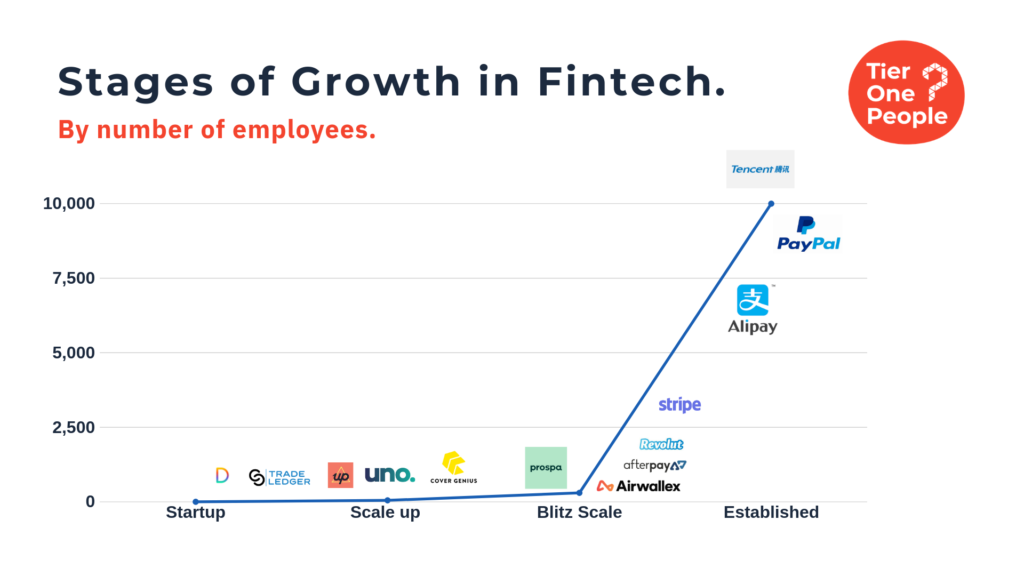

We have created some typical profiles to give context.

Usually 1 - 50 people with minimal funding or bootstrapped (self-funded). Generating some revenue but not much. Likely to still be working out of a coworking space or innovation hub. The business is still at a volatile stage and uncertainty remains around long-term success.

Typically 50 - 300 people big. Likely to be well funded or listed and generating significant revenue. Moving out of startup and starting to become an enterprise. A mix of the founding team and new hires coming from more corporate backgrounds. Potential to hit Unicorn status.

300 people plus, going global and hiring at a huge rate. Now way past unicorn status. HUGE investors onboard. Examples Revolut, N26, Klarna, Afterpay.

The secret to success when joining a Fintech is to get on board when your skills and experience can make the most impact. When we do see hiring fail it's usually not because the wrong person was hired. But the right person is hired at the wrong time.

Have a mortgage or family commitments? You may want to think about joining a business in blitz scale mode. There is likely a lot more security and a higher base salary can be offered with some ESOP. But you have probably missed out on the opportunity to become a millionaire!

Can you take one or two risks financially if the role doesn't work out? Maybe you are not quite sure if you can adapt to the demands of a startup. Try a scale up.

If you are slightly bonkers, can handle flexible working ie working 24:7 thrive on uncertainty, fear, challenge and building a legacy while not getting paid much then a startup might be right for you.

Most people think that Fintechs are one huge innovation lab where people ride round on skateboards dreaming up how to use blockchain to solve world hunger.

In reality most Fintech are struggling just to stay alive. If you are dreaming of bringing killer ideas and strategising all day long, forget it. Having ideas and making ideas happen are very different. In a Fintech you need to bring relevant skills to the table and demonstrate where you can execute on the vision with minimal resources.

Most Fintechs started out by hiring mates or mates of mates. It stands to reason that when it is your business you want to hire people you can trust to deliver.

75% of the Tier One People network will find their next role through a direct contact. If you don’t have any friends in Fintech then you need to make some.

I am constantly amazed by people who tell me they are passionate about Fintech, yet know nothing about the sector. At Tier One People we live and breath Fintech. But we have to work hard to keep building our profile and build our knowledge base. Meetups and industry events are a great way to get started if you need to gain knowledge and meet people.

Fintech is a tight-knit community and you will find many members are quite accessible when you contribute to the community in a positive way.

Technology and global markets seem to be moving so fast, most executives are struggling to keep pace. Couple that with the changing regulatory landscape and looking further than 12 months into the future is creating indecision. When decisions are finally made, the market has moved on, the goal posts have changed and so the process starts all over again!

The answer is no if we look at investment numbers. But we are entering a new evolution, Fintech 2.0 and the platform play. The pressure is on for founders and executives to deliver to investors and shareholders. The challenge for scaling Fintechs appears to be plateauing top line growth or even an obsolete product/business model.

Most Fintech to date are apps/features or middle layer software solutions. But with the emergence of 'Super Apps' like Revolut the competition is becoming much tougher. And customers expectations are rising.

When it comes to scaling the business two options are most often considered. Grow geographically (Cover Genius and AfterPay have taken this approach) or pivot domestically. To pivot successfully requires two things; new products and people to drive the sales of new products.

Pivots are not exclusive to scaling startups. We see an increasing demand for Fintech talent from corporations pivoting their own product lines. Some are even reinventing their business models. Some examples include FSI’s, Insurers and Software companies.

Based on our assessment of the market there is significant demand for two profiles from Fintech.

Founders and business leaders seem to be crying out for commercial product managers with the ability to deliver the killer product. Indeed, the EY/Fintech Australia Census 2019 highights Product/Market Fit as the number one challenge for Fintech.

Product areas appear well stocked with those who can project manage. Strategic and commercial acumen seems to be in short supply, leading to months wasted on product development before a market fit has been established. Business leaders dream of applying Lean Startup Principles. While Product teams seem obsessed with following Agile rather than being Agile.

2019 has seen an increase in Head of Product and a Chief Product Officer searches at Tier One People. We sourced 75% of shortlisted candidates domestically. 25% were international candidates. However, it is a 50/50 split on domestic and international hires made.

Based on the client feedback, it was felt international candidates demonstrated clearer commercial thinking. Most importantly, talent could point to several examples in which they had taken a product from idea to revenue generation, at scale.

It seems the product management community is acutely aware of the problem. Read this excellent blog post by Adrienne Tan https://brainmates.com.au/product-management/cut-out-product-management/

Revenue growth is hard to come by and the pressure is beginning to show signs. The sizzle of Fintech has attracted a lot of investment. Indeed 2018 saw an all time record for Fintech investment in Australia. And with the additional investment come higher expectations.

I wrote of this phenomenon three years ago, when SaaS businesses went on huge hiring sprees for business development managers.

We are seeing increased demand for people who can bring in new business. Especially significant corporate partnerships that will make an immediate and long term impact on revenue growth.

B2B sales is complex. Deals can take anywhere from 6 - 18 months. B2B2C deals may not take as long, but with API integration to be factored in, there is a heavy dose of project management required to onboard any new client. Deals are fragile and complex with technology and regulatory roadblocks often leading to months of work being wasted.

The market is reacting with an increasing demand for Partnerships Directors. These are rare people indeed. A Partnerships Director must possess the hustle and entrepreneurial drive of a sales person. But with empathy/relationship building and well developed project management skills. If that wasn’t difficult enough to find, strong product knowledge and hands on operational experience is considered essential to the role.

Tier One People have had success sourcing talent from the UK and US markets which are more accustomed to this model.

Our clients seem to be experiencing better outcomes by adopting a design thinking approach to hiring. Over the last year we have been working with a small group of trusted clients on a new approach to recruitment. It has been so successful that two clients saved close to $500,000.

If you would like to find out more, get in touch to organise a consultation.

2019 is shaping up to be a HUGE year for FinTech in Australia. But where is all the FinTech Talent to help you grow your business?

Together with our partners, clients and good old market research we have compiled a list of the most in demand skills. FinTech startups can’t match the salaries of well capitalised businesses and often struggle to hire the talent they need. We have excluded startup data from our research and have focussed on companies series A and beyond.

Banking and Financial Services Software companies have big plans in 2019. Established banks will look to defend their position as Australia goes Neo Bank crazy. Large international players now see Australia as a major strategic play as open banking puts Australia on the map for innovation.

New banks means new clients requiring core banking systems, lending platforms, security, CRM, Analytics. An endless list!

Sadly, there is a serious lack of sales talent out there. Expect to pay $180,000 as a base salary for anyone with 5 years-experience enterprise software/SaaS sales. But don’t expect too much in return for your money. Most sales people change companies every 12 – 18 months. In an environment where deals can take anywhere from 6 -18 months to complete, even at $180,000 you won’t get a deal closer.

If you are looking to grow your FinTech business by hiring someone who can close deals with Banks and Financial Institutions, expect to fork out $220,000 plus bonus, benefits and LTI, if you want to see results. Take a look at this advert as an example.

FinTech’s with a B2B or B2B2C model require Account Directors who can win new business and act as the link between the tech team and client. So, they created the Head of Partnerships role.

Part Business Development, part Account Management, to secure the best people for this type of role you are looking $180,000 - $200,000 plus bonuses/benefits.

As this is a fairly new role to the Australian market, talent from advertising and media agencies can often present the best skills match. Alternatively we find talent from the US and UK are accustomed to this model and will often make the best hires.

Are the days of the CMO numbered, a slow death by 1000 (job) cuts? Marketing today is all about growth - ROI and the numbers don’t lie!

Sales and Marketing, especially in B2B models is returning back to its origins, one integrated and seamless function. The revenue generating engine room of the business. The challenge lies in finding people with a broad base of experience, that encompasses Product, Sales Pipeline, Digital Marketing, PR and Brand.

$225,000 plus super and bonuses is the starting point for a capable CGO who will deliver results. Expect to pay more depending on the size and scale of the role.

Judging by the feedback from clients and the market, it seems many FinTech’s are considering a pivot or growth into new markets. We have held a number of discussions over the last 90 days with clients looking for a similar profile. A Head of Product Development who can change Product teams focused on process ( and who seem convinced that applying Agile methodology solves everything) into product development teams shipping product that sells.

The right person typically comes from an engineering background. They break the mould by demonstrating commercial acumen/results and an ability to change the behaviours and beliefs of product teams.

Expect to pay anywhere from $180,000 plus benefits and bonus for this type of person. Our research suggests they will be in big demand 2019, no doubt the figure will rise.

As the challenger banks officially launch in 2019, the thing that keeps CEO’s awake at night (apart from trying to get a license) is security. Ironically, the best Cyber Security people I know don’t class themselves as Cyber Security specialists. They are risk experts.

If you are on the hunt for a Cyber Security specialist expect to pay big dollars. Or go to the source, Eastern Europe and hire the people who are your potential threat!

No change there, each year it gets harder. I heard Google recently paid an engineer in London a $3m salary. Expect to pay what you have to pay to get the right person. It is extreme, but we have plans underway to help the FinTech community access top development talent on reasonable salaries!

AI continues to be the buzzword of 2019. Will it follow the same path as Blockchain? Business leaders are beginning to recognise the limitations of Ai and the potential business issues it can cause.

Instead of replacing humans, the buzzword of 2019 will be ‘augmentation’ as we seek to automate mundane tasks. The emphasis will be on machine learning. Hardly ground breaking, we have been doing that in the workplace since the industrial revolution!

Still, a great data scientist will cost around $150,000 in 2019. And if you want a genuine AI/ML specialist, our research team is scouring the universities and colleges around the world.

Fintech is one of the hottest employment sectors. With banking and financial services facing HUGE disruption and so many banking and financial services execs entering the Fintech job market, there is increased competition for opportunities.

When Tier One People does advertise a role, we receive 150 – 200 applications on average. Couple that with a market search and on average you are competing against 300 plus potential candidates. How can you give yourself a competitive edge and ensure you are the one securing the dream move to Fintech?

I've been in the recruitment game for over twenty years. Over that period, I have given career advice to 25,000 plus people and helped thousands of people find a job. I've worked with hundreds of clients.

Putting all of this experience together I've developed a simple approach that helps people accelerate the job search and maximise their career options. The system in many ways follows the principles of Product/Market fit applied in Lean Startup methodology developed by Eric Ries. The distinction here is YOU are the PRODUCT/Service and a potential employer is a CUSTOMER.

The most common mistake I believe people make when thinking about any career move is who they FOCUS on. When contemplating the next step, we have been conditioned to ask questions such as

‘What am I looking for?’, ‘What will make me happy?’ ‘Where do I want to be in 5 years-time?’

I see a big issue with this line of questioning. What you want is not the focus of a potential employer at this stage. What every employer is focussed on is solving their problems.

The first step of any job search is to ask yourself one simple question.

“What is the BIG problem I solve?”

This is a critical step. If you are solving problems Fintech’s don’t have or don’t see as a problem then the job search is going to become tough.

Typically, we see people moving out of a large corporate environment promoting their expertise in Innovation or Transformation. These problems are prevalent in big banks, but not such an issue in a Fintech startup.

The growing adoption of AI and rapid advancements in technology mean it's very easy for tasked based skills to be considered less important. And the focus is shifting to people's ability to make an impact and deliver outcomes.

Even if a FinTech needs your solution, will they use your service, or will they use someone else? There is a lot of competition out there. Are you as good as, if not better than your competitors?

If not, what areas need improvement to make your product the market leader?

In most instances’ businesses are experiencing one of three problems. Over the years we have come up with different terms, change, transformation, strategy, sales, product fit, disruption. But ultimately, most problems facing a FinTech founder can be distilled to the following:

REVENUE - Sales and Growth

SCALE - Operational efficiency

Ultimately your product (YOU) may have one or two benefits to a FinTech. You can demonstrate where you can GROW revenue and/or SCALE a business. People who demonstrate the ability to drive revenue and scale are naturally in the greatest demand because they will have the most IMPACT on a business.

A Fintech startup will usually hire the person they feel will make the greatest impact immediately.

It surprises me how few people know or can estimate their value to a business. I often hear the term “Value Add” dropped in resumes and interviews. Yet when I ask how? I am met with a blank stare.

The Lean Startup talks about the Value Hypothesis Test which determines whether a product or service truly delivers value to customers. As you are the PRODUCT, I recommend a simple value creation exercise to determine the value you bring to a potential employer.

List your career achievements and attach a dollar value.

As an example, you may have automated a process, which resulted in a reduction of head count, saving costs. If you managed to reduce headcount by one and that person was on a salary of $100,000, over a five-year period, you have saved the business $500,000. In other words, you have created $500,000 worth of value.

Repeat this exercise for every notable contribution you have made to a business and total the amount.

You might be surprised how much value you can bring to a FinTech startup.

Most job seekers spend 100% of their time and energy with a go to market strategy that doesn’t fit the customer.

The typical job search mirrors a B2C marketing campaign. High volume, low touch.

You've applied to hundreds of jobs on line, you tick all the boxes, yet don’t even get a response. You meet multiple recruiters who said you were perfect for the job and you never hear back.

This high volume approach rarely works, especially when your are targeting the wrong person.

A job search should mirror a B2B marketing campaign, low volume, highly targeted with multiple touch points. You need to find a way to get in front of your customers and pitch your solution.

Evan Wong, CEO of Checkbox.ai (RegTech of the Year 2017 and 2018) has this advice:

I had to grow our network of Tier One clients from nothing. Coming straight out of University, I had no existing contacts or network in Corporate land. So, I started out by creating a general profile of people I thought that would be interested in the product. Through a combination of research, Google searches, reading articles, blog posts and LinkedIn profiles I built a target list of ideal customers.

Next, I’d reach out by email asking to set up a short call for feedback, not to sell anything! Just feedback on the Checkbox value proposition. The discussion would usually be followed up a few months later with an in-person demonstration of the product. At the end asking for recommendations or referrals to other contacts in their network.

Today most of our business comes from word of mouth and thought leadership marketing. Being active at industry events and conferences helps our profile a lot.

Moving straight out of corporate and into a FinTech startup is tough. Especially in this market. You are likely to face lots of rejection. Does this mean you should give up on a move into FinTech?

Don’t despair, this is where you might want to PIVOT or change your strategy. Feedback from interviews and meetings with potential employers can help form the basis of your Pivot.

It may be you need experience in a smaller business before a FinTech startup is comfortable hiring you. A credit union, mutual, or smaller bank undergoing digital transformation can be a great stepping stone to a FinTech.

Could there be opportunities in your current employer that will help you build your skills and experience?

A corporate venture fund?

An acquisition of a fintech startup?

Maybe you just need to PERSEVERE. The key here is to immerse yourself in the FinTech ecosystem. It is what I call Proximity. The more people see you around the FinTech scene the more likely they are to offer you a job.

Go to FinTech meetups, attend events, keep in contact with Founders, post relevant content on Linkedin and Twitter, start following the people who have a profile, look for opportunities to help and connect people.

Follow these steps and before long you will find your Tribe, doing game changing work with amazing people.

Artificial Intelligence and machine learning have advanced to a point where almost everyone in the Insurance industry is asking – 'Is my job at risk?’

The answer? Nobody knows for sure. However, based on our extensive research and the daily discussions with insurance industry experts, expect to see the beginning of changes in 2018.

Many of the articles published in the media are highly exaggerated and designed to cause panic. However, AI and machine learning technology has reached a point where most traditional, task-oriented jobs are in the process of being replaced. Industries including Banking and Insurance are undergoing seismic shifts that demand new skills and a new approach to the workforce.

We recently spoke with Insurance leaders across the globe to get their views on Artificial Intelligence and the role it will play on the industry.

Here is what they had to say.

There are huge implications for machine learning and AI that will eventuate in the next couple of years. Without a doubt, they will have a big impact on how insurers run their business.

Insurance is a data business and always has been. What's changing is the breadth and type of data that is becoming available to insurance companies.

Insurance companies have a great capacity to analyse data and crunch numbers. Risk and pricing models and the associated skill sets are becoming outdated.

Let’s consider how an insurance company approaches underwriting and pricing. They collect a huge, historical data set and then analyse the data to create a product. Companies like Trov are very different. Using AI, we collect real-time information on how customers interact with the product. We can pull in data from multiple different sources.

So, the question we ask ourselves is 'How can we use dynamic and real-time data to deliver better products and pricing.’

Do large Insurers have enough capability in this area? Many Insurers have closely held biases towards the historical data they collect. Sometimes they struggle to wrap their head around how they should price products for example.

The technology available will change the nature of traditional roles in claims, underwriting and actuarial. But I don't think Artificial Intelligence will replace these roles. It is more likely the roles will continue to morph and cross pollinate.

Rather than replace people, we think we can support our clients by experimenting in areas like Artificial Intelligence and Machine Learning.

As an example, we are helping clients with text mining on claims to better analyse their data using robotics. This gives our clients greater insight into their claims experience and history which in turn drives better focused propositions.

In Korea, we are working with an AI partner and a specialist hospital to develop a data base which can be used to develop future products covering important conditions not currently covered.

In the US we have developed an underwriting algorithm based on the use of multiple data sources replacing traditional underwriting methods. All have been developed in conjunction with and in support of our insurer clients. The industry really is leading the charge and demonstrating that it is determined to stay relevant – and doing a good job at it too. Our people are a huge part of the success, technology is just helping us do a better job, faster.

Artificial Intelligence and Machine Learning is having an impact in our business; however, I see technology helping our people to do their job rather than replacing them. I don’t see the current disruption trend to be any different than what we saw 25 years ago when organisations began to digitise processes and increase the use of computers in the workplace.

We are investing in the transformation of our claims service, including the development of a new claims team in Australia, to improve the customer experience. We recognise that certain types of claims, such as householder claims, require a high level of personal contact, specialist knowledge and a rapid resolution for our customers.

The introduction of Artificial Intelligence/Machine Learning will speed up the claims process even further and we are in the process of piloting innovative technology across our business.

As an example, we have recently partnered with Risk Genius, an Artificial Intelligence/Machine Learning tool that allows the user to examine policy wordings. We have thousands of policy wordings in QBE, and without a tool like this it would be a very manual task to compare two or more policy wordings

The Risk Genius tool enables the user to instantly find the differences, which helps us create contemporary policies and release new products to market much faster. This is an example of people working with machines rather than machines replacing people.

We are also pioneering Artificial Intelligence/Machine Learning in our business to transform our capacity to assess bodily injury claims. We have partnered with an organisation to give our claims managers access to data to better manage the claim. This pioneering technology is something we have been using in the US, so we are excited to introduce this new way of enhancing the customer experience.

Finally, the views of an Ex- McKinsey Consultant who asked not to be named due to client confidentiality.

Artificial Intelligence is already replacing people in many insurers. I expect to see two waves of change.

The first wave of change will happen (and is happening) in contact centres. There is a rapid rate of adoption with chatbots. Go on any website of any tech company, and a chat bot will serve you. Most Insurers are in the process of adopting the technology.

The second wave will impact around 50% of jobs and professions.

Accounting, claims and underwriting, financial analysts, risk analysts, low-level sales, operations. This is just a sample of the roles we can expect to see impacted by AI.

Any low value, transactional role is at threat. As an example, if you are assessing low-level claims or underwriting low value, generic policies then expect to be replaced by Artificial Intelligence.

As a recruitment business, Tier One People are perfectly positioned to assess the job trends. It appears, for the moment, AI is not leading to large scale redundancies.

If you are a specialist underwriter or actuary, then your job is safe for the next few years. But the technology is advancing at a rapid rate, even these roles could be performed by AI in the future.

The roles that will be safe are those reliant on interpersonal skills and human interaction, high-level claims, sales and relationship managers and executive or senior management roles.

There is huge demand for Regulatory and Compliance specialists, Software Developers and Engineers, Data Scientists, Machine Learning Specialists, Business Intelligence, Community Managers for social media, Health and Wellness experts.

At a senior level we are a seeing newly created executive roles such as Chief Customer Officer, Chief Innovation Officer, Head of Ventures, Chief Strategy Officer.

InsurTech thought leader, Matteo Carbone recently published a book titled ‘All the insurance players will be Insurtechs’

The hiring trends Tier One People observe within our Insurance clients suggest Matteo is 100% on the money in his assessment.

So, rather than asking ‘Will AI replace my job?’ perhaps we should ask ourselves ‘What role can I play in an Insurtech?’

At Tier One People, we get to work with some amazing startups in Fintech. January has got off to a flier, so here is the first Tier One People Sydney FinTech jobs update of 2018.

There is an air of optimism that Fintechs will be a success. But the two challenges facing every FinTech and InsurTech? Funding and hiring great people.

The funding issue may no longer be an issue. Last week saw Australia's first ever crowdfunding equity raise. The raising for Xinja (Australia's first NeoBank) was carried out by Equitise. AUS$500,000 was raised in one day and everyday Australians (like me) have been given the opportunity to be an early stage investor in what promises to be a super exciting venture.

Congratulations to Eric Wilson and Van Le of Xinja and Chris Gilbert of Equitise.

Last month I had meetings with CEOs, CROs, CMOs, CTOs, CFOs and COOs. Each of them described similar people challenges - namely, hiring people who can get results in a VUCA environment with limited resources.

Interestingly only CTOs mentioned technical skills as their biggest problem (even then they can outsource). As one CEO put it, 'I need people who are prepared to work seven days and can get sh!t done.'

It is clear that the education system and corporate structures are failing to prepare people for the new demands of the startup/high growth business model.

If you are serious about a career in Fintech, then you need to master the art of 'getting sh!t done'. Despite what you read in the press, startups are not all about free yoga, beanbags and as much alcohol as you can drink.

Thinking about a move to Fintech? Tier One People are running a free event in February for those looking to make the switch. Contact dexter@tieronepeople.com for details.

There has been a push recently to hire Financial Controllers and CFO's within the Fintech space. With companies growing to enterprise level in record time (Uber started in 2009 and is now valued at $70bn), startups are recognising the need to invest in enterprise-ready infrastructure and finance functions.

Several of the mandates I have received in the past few months have been with companies less than two years old.

A big year for risk in 2018. Valuations Actuaries, Cyber Security and Regulatory Compliance people in hot demand.

No change here.

Full stack developers - Yaaaawwn.

Machine learning, Data Science and Analytics still in huge demand.

Blockchain - Expect to see a raft of specialist recruiters in Blockchain.

The interim C Suite market is going strong. Have you ever considered utilising CXO services on a 'pay as you go' plan for instance?

If you are looking to grow your Fintech and need specific expertise, for events such as an IPO, acquisition or rapid growth, hiring the person you need is cost prohibitive. Tier One People connect Gig Execs to our Fintech and Insurtech clients. A Gig Exec is a highly experienced executive with specialist experience for specific business events. Readily available for short-term assignments, this is a highly cost-effective solution for FinTech founders requiring executive level support.

It turns out that making revenue from SaaS and platform solutions is rather difficult, especially if you are relying solely on PR and a digital sales strategy. Tier One People are seeing an increase in demand for Sales Directors and Business Development Managers.

Interestingly the ideal candidate is someone with broad experience in product, distribution and sales. Relationship building and strategic selling are an absolute must. Certainly no used car salesman! It seems the mantra 'People buy people' is truer than ever.

A great initiative by Cameron Dart and Australian FinTech Jobs, a specialist jobs board for Fintech positions. We have used the platform for several positions and the quality and relevance of candidates gets high ratings from Tier One People.

We always say to our clients hire yourself if you can and when you can't come to us.

Australian FinTech Jobs is generating better results for Tier One People than SEEK (and is a lot cheaper too.) If you are planning to hire direct, I recommend giving the platform a go.

Without a doubt, the most rewarding aspect of being a recruiter is working with the best talent. Seeing the positive impact a great hire can have in a business is a privilege. And I have been fortunate to play a small part in the success of some amazing companies (some of whom are now multi-billion-dollar businesses).

Founders of FinTechs will know more than most, the damage caused by making the wrong hire. Especially when a business is in the earlier stages of growth.

If you are a growing FinTech, finding the time to recruit yourself is tough and throwing your capital at recruitment companies should be a last resort. Technology, social platforms and a 24/7 connected society has made finding candidates a lot easier. The challenge lies in engaging, assessing and finally hiring the right people.

What is the biggest obstacle preventing you from hiring the right people?

Recruiters, job boards, a lack of talent?

All of the above can be contributing factors. But the number one issue leading to a failed hire is this.

The hiring strategy, or lack thereof.

Hiring becomes much simpler and faster when you have a clearly defined hiring strategy.

In most instances, FinTech founders engage Tier One People after a failed attempt hiring themselves. When we take a brief, the client's job description reads more like a wish list. The client has spent six months looking for a Unicorn with blue eyes. The longer the search goes on, the more pressure the client feels, leading to poor hiring decisions.

Developing a hiring strategy may sound too ‘hard basket’ but it is a lot simpler than you may think. You can even apply design thinking principles to your hiring strategy by asking a few very simple questions.

What business problem does this hire solve?

What does the right person look like?

Where can I find them?

What compelling reason can I give the right person to join our business?

None of the above questions are answered by a conventional job description.

It is very likely you have spent a lot of time, energy and money creating a company brand and customer experience to attract the right customers. How much time and energy does your business spend creating a brand and candidate experience that attracts and retains the right employees?

Why would a top performer be interested in working with your FinTech?

What is unique about you and the business you are creating?

Why choose you over another business.

What is your unique value proposition?

What does it mean to be a part of your organisation?

A candidate experience strategy is best developed at the very early stages of growing the business. Unfortunately, most founders leave any form of recruitment process until the business hits the high-growth stage. Hiring becomes problematic, multiple recruiters are engaged, cost per acquisition goes sky high and cultural issues start to appear.

This advice goes against everything we are taught, even by the legend Peter Thiel himself. But here is my question ‘What is culture?’

The culture of an organisation is not static, it evolves and changes with the business. Culture is a living, breathing, growing animal. At the early stage of business, culture is like a baby, yet to develop an identity. It is almost impossible to identify culture fit; however, it is possible to determine if a new hire will add to or enhance your culture.

'The culture of any organisation is determined by the worst behaviour the CEO is prepared to tolerate, in themselves and others.'

If you are the CEO/founder, then the culture will ultimately be determined by your values and behaviours.

Of equal importance are the behaviours you will NOT tolerate. Establishing clear boundaries and guidelines will help when it comes to making tough decisions and assessing cultural fit.

Listing your values is much easier than coming up with a corporate bullsh#t culture statement. My kid's school has cleverly distilled their values and expected behaviours into the moto 'wisdom and courage'.

You need plenty of both working in a startup!

Most hiring tends to be a knee-jerk reaction to an event or workload. With tight deadlines and a business to run, FinTech leaders have little time to think about the type of person you need to hire.

Tier One People apply a design thinking approach to hiring. That is, we look for the business problem behind the hire. Once we are clear on the EXACT problem we are trying to solve, we can then find the right person. This approach has reduced our average time to hire for leadership positions to four weeks NOT four months.

Once you have identified the business problem a new hire needs to solve, start building a profile of the ideal fit for the role.

What qualities, behaviours and values will they demonstrate on a consistent basis?

What characteristics are required to be a success in the business?

What kind of achievements and results can they point to?

How does this profile compliment the dynamic of the current team?

How long will the person need to perform the role for?

Contemplate where your new hire will fit in the business 1, 2, 3, 4 and 5 years from now. It may be that the profile you have identified will only fit your business for 6 or 12 months. That is perfectly reasonable, especially as your business goes through rapid growth.

Job descriptions list daily tasks and responsibilities. They were perfect in the last century when people worked static jobs in static environments. Today people live and work in a VUCA (volatile, uncertain, complex, ambiguous) world. Jobs and businesses are anything but static. No two days are the same in a startup and employees job description change on an almost daily basis.

The person you need to hire is likely to be in a great role already and not thinking about a move. For them, the prospect of moving to a startup just to do the same job is not a compelling proposition. And the right person will not ask for a Job Description. They will do whatever it takes to get the job done (as long as it is legal and ethical.)

Put your marketing hat on and create avatars of the people you want to hire. Outstanding people aren’t looking for another Job, they are looking for a compelling opportunity.

What stage of life are they at? Who are their friends? What is frustrating about their current job? What inspires them? Who do they aspire to be? What is important to them? Friends? Family? Adventure? Travel? Prestige? Alcohol? Table Tennis? What is their work ethic?

Having a detailed picture of your ideal hire will help you create an opportunity description that is compelling to the right person.

It is actually much simpler to create an opportunity description than it is to create a job description. Start off with a set of goals, targets and milestones to be achieved within the first 18 months. For example:

- Within the first six months implement a new billing system with full integration of sales systems and no bugs or errors.

- Within the first 12 months have hired and groomed a potential successor into your role, enabling your advancement into a managerial position.

- Within 18 months have contributed cost savings in the business of $100,000 by identifying outsourcing and automation opportunities.

Incentivise each milestone with bonus, equity or promotion to make the opportunity even more compelling. Every new hire will have absolute clarity on what is expected of them and you have a congruent performance management framework in place before the person has even started the job.