Will AI replace people in banking?

An opinion piece by Dexter Cousins, Managing Director of Tier One People.

In late 2022 Chat GPT seemed to come out of nowhere, the truth is the technology is 7 years old and advancing at a rapid rate. Companies have been developing AI tools for decades, and in the last 10 years we've seen a huge increase in the adoption of AI in business.

So why is everyone suddenly scared that AI is going to take their job? I originally wrote this article back in 2017 and have come back to update it several times.

Will AI replace people in banking?

It is a question I am asked everyday. Now if you had asked me three years ago my answer would have been 'no.'

Today I am not so sure, in fact I am convinced technology will replace up to 80% of jobs in banking.

While it is just a theory, it is not one I have plucked up from thin air. Nor is it based on wild claims about the capability of AI. This post is not intended to alarm people, but there are forces at play that when I follow through to a possible conclusion, there's a very real danger to jobs and our careers.

The Future of work.

Since 2012 I have been absorbed by the changing nature of work. My interest was piqued when I heard about a company called 'Freelancer', a platform connecting knowledge workers around the world.

Ever since I've spent much of my time researching and analysing the disruptive nature of technology, AI and robotics in the workforce. And yes I am worried about my own existence as a managing director of a recruitment business.

And this fear drove me to reinvent my own career, business and approach just to remain relevant. Ultimately I set out to create a business that was recession-proof and could be operated from anywhere in the world with a smartphone and internet connection.

Since Covid hit and remote working has been forced upon us, the term ‘The future of work’ is repeatedly used - but the future is here and has been for some time.

What we are seeing now is a tidal wave of change that has been building up for decades, multiple forces are converging that threaten very rapid change which humans are struggling to keep pace with.

In this two part piece I'll cover the forces and share why I believe they will make 80% of banking staff redundant.

Force one: Purpose-built digital banks create pressure for boards and CEO’s.

There's a lot of debate about Neobanks and if they will succeed. There seems little concern from the incumbent banks that Neo's will ever get the scale to threaten their profits. I feel this is a rather short-sighted and narrow view of the threats.

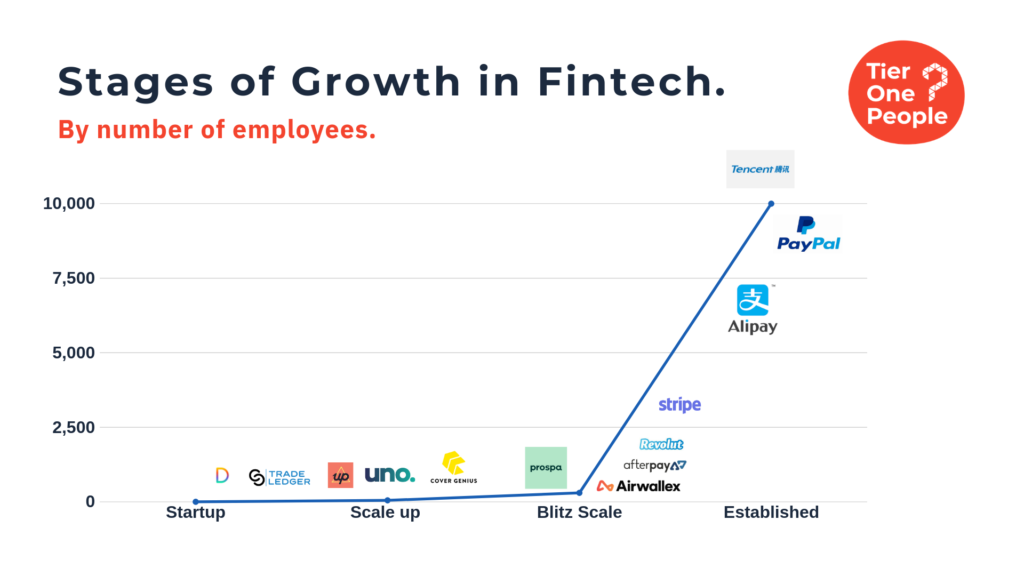

Australia’s leading bank, Commonwealth Bank, was founded in 1912. It serves approximately 10m customers across retail and business banking mainly across Australia. The bank employs approximately 52,000 people and in 2020 made a net profit of Au$7.3bn or a profit of Au$146,000 per employee

As banks go, they are at the forefront of digital innovation and easily in the top 10 banks globally when it comes to digital. They took the bold step of replacing their core banking system in 2008 and are currently in the process of moving 95% of technology and apps into the public cloud.

Revolut. Some would argue is not a bank although it does hold a European banking license and is in the process of applying for a UK banking license. Launched in 2015, in just six years Revolut has gained 14m customers with operations in the UK, Portugal, USA, Japan, Singapore, India and Australia.

It offers customers low cost international transfers, access to gold and silver, cryptocurrency, free share trading and in the UK also offers business accounts. Revolut develops products and ships features at a lightning pace, operating more like Amazon than JP Morgan.

Revolut currently employs approximately 2000 employees and is now operating at a profit.

What is not clear at this stage is if Revolut's model will generate big profits like CBA. In order to be as profitable as CBA per employee, they will need to generate Au$292,000,000 profit.

Revolut does not yet offer lending products, which are the most profitable products in any retail banks portfolio. But when Revolut does start lending, how many additional people will they need to employ?

Definitely not 50,000.

Is Revolut a one off? No, in Hong Kong, Welab has approximately 800 staff and serves 40+ million users/customers.

As more companies like Revolut and Welab gain momentum, increase revenue and exponentially increase profit, surely boards have to question why 52,000 are needed to run a bank?

In Australia we have witnessed 3 CEO’s lose their job in the last two years, all to mishaps in risk and compliance and ultimately human error/interference. The logical conclusion to draw - if processes can be automated to remove the potential risk of human error they will be.

Force two: Remote working and cloud.

Most banks are listed on a stock exchange, meaning their no1 goal is to generate profits for shareholders. And in order to remain profitable incumbent banks will need to replace people with technology. Shareholders expect returns and dividends and every CEO is incentivized to deliver.

When you already have the lion's share of the market, the only way to deliver more profit is to cut costs. And people are usually where the biggest cost savings can be found.

Many banks are focused on replacing legacy systems and moving to the cloud. Covid19 has accelerated this trend. But could a move to the cloud lead to job losses and displacement?

We have to anticipate that more efficient technology will lead to job cuts, particularly for those who's jobs are based on data input and spreadsheets. But there are greater implications

Commonwealth Bank is ahead of the curve having replaced the core banking system and moved to the public cloud. Matt Comyn the CEO is intent on delivering a new experience for customers. And to help he is bringing in the very best talent from the startup and Fintech world.

Developers, engineers, cybersecurity, blockchain, data science. The list of talent suggests CBA identifies itself as a silicon valley tech giant, much like Google, Facebook and Netflix.

As more and more banks replace legacy systems and move to the cloud their demand for similar skill sets will increase. We are seeing this with other digitally savvy banks like JP Morgan and Goldman Sachs.

The demand for these skills is high, but supply is low, especially if you look locally. Here in Australia we see comparably average software developers with 2-3 years experience commanding $200,000 per year. In the past many banks have made do with local talent. Now they are looking globally for the very best talent in the market.

If you go to India or Eastern Europe you can get incredible developer and engineering talent talent for a fraction of the cost. With a move to cloud banks realise many of their staff can work remotely, which means technically a job can be done anywhere in the world.

This potentially threatens local jobs in two ways.

- Lower skilled workers miss out on the opportunity of higher skilled jobs and salaries to highly skilled talent overseas. Without the need for Visas, work permits, travel, relocation etc employment costs can be drastically lowered.

2. If a job can be done remotely, technically it can be done anywhere in the world, meaning cheaper labour is available. Will lower skilled workers miss out on the jobs they are qualified for to overseas talent who can perform the same tasks at a fraction of the cost?

Force three: Artificial intelligence.

There’s a recent trend where offshore jobs have been brought back onshore. One area we’ve seen this most is in customer service, especially since Covid. Bank branch staff have been repurposed as customer service/contact centre staff.

This is good news in the short-term. But there’s a looming risk to jobs. We work with several Ai companies who work with banks and are in the process of automating customer service. Working closely with the customer service staff, actions are input into Ai/Machine learning models and emulated.

I’ve personally seen trials of the technology and it is scary how good it is for dealing with general enquiries. I was on hold for 3 hours to my bank last week for a simple inquiry that’s still not resolved, waiting in a queue for a human to answer!

Artificial intelligence is being adopted in Customer Service, Risk, Pricing, Compliance, Finance, Treasury, basically every area of the banking industry.

While it will never replace humans completely it will take away many of the mundane and repetitive tasks. It’s feasible that a department of 50 could become a department of 5 SME’s supported by a data scientist and Ai.

Force four: Open Banking and CDR.

The promise of CDR (Consumer data Right) is some way off. It’s an ambitious plan to give consumers the right to use their data for their benefit. Imagine applying for a mortgage and getting unconditional approval in minutes. That is the promise of open data.

Initial progress is slow, but don’t underestimate how fast things will move once there is traction. Tier One People is working with well-capitalised startups with a vision to completely disrupt lending.

The applications for open banking threatens jobs on many levels.

The first two jobs at risk are credit and underwriting. With access to my entire past 10 years of spending and online data, credit risk models will be able to give a decision instantly. Just ask anyone applying for a home loan right now if this is something they want. People are losing deposits on houses because it is taking banks 3-4 months to give a decision on an application.

Now imagine a world where you are instantly given a decision and approved. This potentially takes away the need for mortgage advisers, underwriters and credit assessors. And because it is all automated with audit trails, there’s no need for compliance either.

Force five: The next generation of customers.

My kids are 10 and 8. They love video games and can tell you everything you want to know about Neobanks. They closed down their school bank account recently.

“How dare a bank expect me to turn up to school with cash, fill in a deposit form and not let me access my money when I need it”

Now they have a Spriggy account (with cool star wars cards) and Revolut kids accounts. My mum and siblings (living overseas) regularly send the kids money to their Revolut accounts. It hits the account in 30 seconds with no international fees! No waiting 4 days and giving 10-20% to the bank in fees and conversion charges.

They spend most of their money on Avatars in a game called Roblox. You may have heard about it, the company just listed on the NYSE and the share price pretty much doubled.

About half of American kids under 16 are on the platform! So what does this have to do with banking? Quite a bit actually.

First of all the game has its own digital currency, Robux. You can use Robux to buy avatars and play games which other people build. You can even build your own games and get paid Robux when people play your game.

The world my kids are growing up in is a one where they don’t trust banks, they don’t see a need for banks and they are very comfortable with digital currencies and storing them in digital wallets.

We are living in a world where businesses are built almost overnight if they fit the needs of customers. If they don’t, they go bust just as quickly. Blackberry is a great example.

There is no way my kids will tolerate being on hold for 3 hours because of legacy system problems. They will just close the account and go somewhere better.

It is this shift in customer behaviour that potentially poses the greatest threat to banking jobs, mainly because banks are in danger of losing their relevance.

When I first started working, I was paid in cash. I never used nor needed a bank account until my employer began electronic transfers of salaries.

But let’s say my kids choose to be paid in Robux or Bitcoin, like the Basketball star Russell Okung. It goes straight to a digital wallet and maybe held in a cold storage wallet. What kind of impact does this have on bank deposits and their capital adequacy?

We have seen the first glimpses of the changing behaviours of customers with the rapid decline in new credit cards. Instead people are choosing BNPL products with interest-free credit options instead of high-interest cards.

As we move to a negative interest rate scenario, it will cost customers to keep their cash in a bank, will we see deposits shift into digital currencies and gold?

If banks get into capital adequacy trouble, will we see consolidation and further job cuts?

In conclusion banks need to evolve like every other industry and technology will disrupt the model. It is up to us as individuals to recognise and anticipate the changes and keep relevant. This requires reinvention and a consistent focus on personal development.

In the next post I’ll share my thoughts on what the future of banking will look like, the skills in demand and how you can reinvent yourself to remain relevant.